With yield curve inversion (10Y < 2Y) the talk of the town in recent days, the narrative proclaims that a recession is imminent. But, that’s not what we see.

For example, if you analyze the right side of the chart above, you can see that the 10-2 spread has surpassed -0.80% and is at its lowest level since the 1980s. As a result, the bond market is screaming recession. However, the three arrows in the middle show that the 10-2 spread moved from negative to positive before the last three recessions occurred.

Q1 2023 hedge fund letters, conferences and more

To that point, little has changed. While the 10-2 spread has risen slightly, the metric remains deeply negative, and its movement does not match its behavior before the last three recessions.

Please see below:

To explain, the 10-2 spread is far from the flatline, and the current narrative is no different than December. Consequently, while it may seem like an outcome is inevitable because everyone is talking about it, the reality is several metrics contrast the recession/pivot optimism.

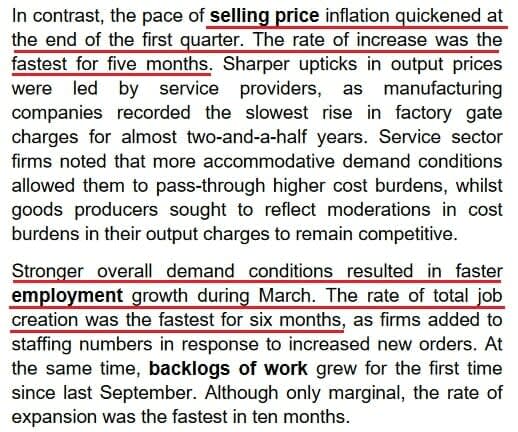

As evidence, S&P Global released its U.S. Composite PMI on Mar. 24, and the headline index increased from 50.1 in February to 53.3 in March. An excerpt read:

“The latest index reading was the highest for almost a year, and signaled a solid expansion in private sector activity…. March data signaled a return to new order growth, with the upturn the first since last September. Although only marginal, the rise in new business was the sharpest in ten months.”

More importantly, S&P Global’s PMI highlighted resilient employment and reaccelerating inflation.

Please see below:

On top of that, ADP released its private payrolls report on Apr. 5. And while the metric came in below the consensus estimate, employment growth increased for small firms and hit new cycle highs for larger firms.

Please see below:

To explain, the orange, brown and gray lines above track the hiring behavior of large, medium and small businesses since late 2019. If you analyze the right side of the chart, you can see that the orange and brown lines hit higher highs, while the gray line bounced after a recent decline. As such, the fundamentals on the ground are much different than the sentiment on Wall Street.

To that point, while employment remains uplifted and the Atlanta Fed’s Wage Growth Tracker is only slightly below its all-time high, U.S. consumers are still flush with cash. We wrote on Mar. 31, 2022:

There is a misnomer in the financial markets that inflation is a supply-side phenomenon. In a nutshell: COVID-19 restrictions, labor shortages, and manufacturing disruptions are the reasons for inflation’s reign. As such, when these issues are no longer present, inflation will normalize and the U.S. economy will enjoy a “soft landing.”

However, investors’ faith in the narrative will likely lead to plenty of pain over the medium term….

U.S. households have nearly $3.89 trillion in their checking accounts. For context, this is 288% more than Q4 2019 (pre-COVID-19). As a result, investors misunderstand the amount of demand that’s driving inflation.

So, while the prediction proved prescient as demand remained resilient throughout 2022 and inflation proved more problematic than expected, little has changed. Households’ checkable deposits have only declined slightly from their 2022 peak and are 362% above their Q4 2019 comparison.

Thus, when you combine this much cash with near-record-low unemployment and near-record-high wage inflation, investors are kidding themselves if they think demand destruction has arrived.

Remember, while silver has been a major beneficiary of the ‘bank crisis means rate cuts’ narrative, this is 2021/2022 all over again. When the crowd attempts to front-run a recession, it negates the recession due to the simulative effect of lower long-term interest rates. That’s why sentiment surrounding silver has gone from euphoric to catastrophic several times over the last two years, and we believe another shift should occur over the next several months.

Overall, the crowd continues to assume that inflation is dead and gone, and this is probably the sixth obituary written over the last 24 months. Yet, each time it rises from the ashes, the PMs suffer mightily and the narrative changes dramatically.

Do you believe the 10-2 spread has merit? Why would businesses hire more employees if demand was so weak? Will consumption remain elevated due to high checking account balances?