Jehoshaphat Research’s short report update on Adapthealth Corp (NASDAQ:AHCO).

Q2 2021 hedge fund letters, conferences and more

Executive Summary:

We are short AHCO and believe that its downside is again around 50%, in large part due to its negative organic growth. However, we no longer have to argue our case with complex arithmetic and assumptions. There is now nothing more to debate – organic growth in both Q1 and Q2 2021 was indeed negative, more than 1,000 basis points below management’s claims. A new SEC filing disclosure confirms it.

This disclosure is brand new, provided for the first time just this past Friday afternoon. In its Q221 10-Q, AHCO chose (was forced?) to disclose its full inorganic contribution to its quarterly results in its 10-Q for the three months ended June 30, 2021. The just-released 10-Q shows an ex-B2B organic decline of -4% for the six months ended 6/30/21:

AHCO quietly uploaded its 10-Q to the SEC website just before 5:30pm this past Friday. Prior to uploading it, AHCO asserted to investors in its earnings release and associated conference call that its organic growth rate was 10%. Analysts published notes celebrating this “fact,” and continue to forecast 8-10% organic growth going forward. The following Monday the company hosted a non-deal roadshow to market its stock and announced the hiring of a new investor relations professional. 10-Qs can get lost in the shuffle under normal conditions, but AHCO seems to have put in some elbow grease to make sure this one did.

On earnings day last week, AHCO stock surged 16% and squeezed out many shorts when management got on its call and proclaimed these silly growth rates. The analyst community breathed a sigh of relief in print, albeit premature. What incredibly awkward timing, then, for the company to quietly release a 10-Q the next day that comprehensively and concisely proves that organic growth is negative after all.

This report is a brief update to our first one, but it is equally important. Here, we will explain what has just changed with the new 10-Q and why AHCO investors are (again) being walked off a cliff by management and Street analysts. And unlike before, you don’t have to do any complex math. You just have to open the 10-Q and scroll down to page 49. Even a sophisticated Wall Street analyst can do that, right?

Full Update To July Report

Management Talked Loudly About “10% Organic Growth” on the Q2 Call and Press Release…

- “As detailed and defined in our Q2, 2021 earnings supplement, AdaptHealth's organic growth for the quarter was 10.1% supporting our long range organic growth estimate of 8% to 10%.” – CFO

- Throughout the call, management threaded the needle through a variety of conflicting, mostly absurd, ideas:

- According to their “pro forma” definition of organic growth, the number is 10%

- Analysts asking about “traditional” or “same-store” organic growth are wasting their time, because it is useless for evaluating their business

- The “pro forma” definition of organic growth is somehow useful in spite of everyone else’s definition being useless

- “Same-store” organic growth is extremely difficult, “almost impossible” to calculate

- AHCO was able to calculate their “pro forma” definition but not the “same-store” definition

- Management also claimed, ridiculously, that they had voluntarily improved their organic growth disclosure in Q121, prior to our report being published. While this is technically true – they did add a nuance of disclosure by quantifying all, instead of just some, current-period deals – it is laughable when viewed in context, because the disclosure added in Q121 did not quantify all contributions and is therefore useless as a barometer of Q121 organic growth. (This is like you asking how tall someone is and getting the answer, “more than three feet.”)

- Sell-side analysts were placated by the happy talk. Organic growth percentage estimates have not budged, and the stock went up 16%. However, just one day later…

…Management Quietly “Admitted” in an SEC Filing That True Organic Growth Was Negative in At Least the Last Two Quarters (Validating Our Methodology for Earlier Quarters as Well)

- Just to be clear: Management has admitted nothing explicitly. What they’ve done is caved to pressure – probably from their lawyers after those lawyers read our report and spoke to other lawyers – to put a complete inorganic growth number into their 10-Q, finally. This is essentially the same thing, but it arguably allows the company to save face by confirming with one hand and denying with the other. (Jim Chanos once called this “differential disclosure” in a widely circulated video about short selling.)

Following are two screenshots:

The first is from the Q121 10-Q (before our report):

The second is from the Q221 10-Q (after our report):

The new disclosure in the latest 10-Q is so subtle that you could almost miss it: The company has gone from quantifying only the revenues contributed by this quarter’s deals, to quantifying the revenues contributed by all deals in the past twelve months. (If you don’t have the latter, there’s no way you can calculate organic growth.)

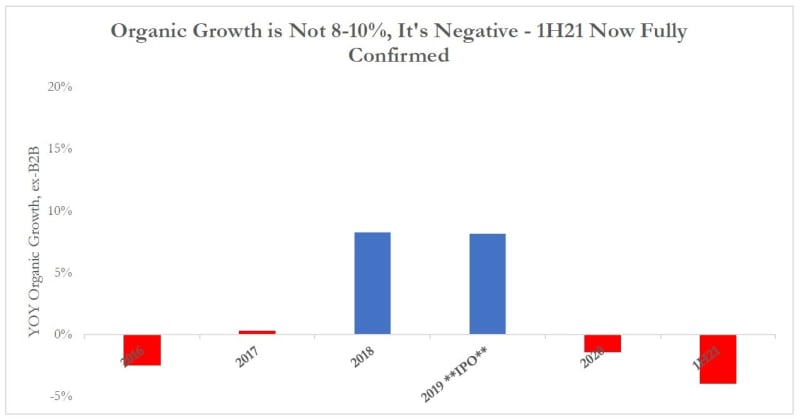

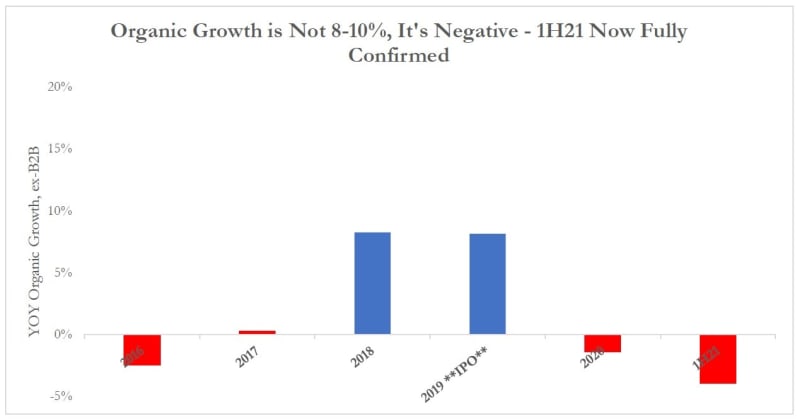

With the new numbers, including the YTD disclosures on Page 1 of this update, organic growth ex-B2B is easily quantified: -8% in Q121 and just under 0% in Q221. Also, we now have further confidence in our original report’s methodology that calculated negative organic growth in Q320 and Q420, and that calculated around zero over time. We knew our math was basically right, but now it’s a little tighter. And as we’ve said before, the best comp to this business, Apria (APR), has low-single-digit organic growth over time. The 8-10% fiction was created to sell stock.

- This new disclosure is enough for anyone to understand with virtually no work done: organic growth for AHCO is flat to (deeply) negative. We didn’t have that ironclad confirmation before. We have it now. From here it’s just a question of when the market begins to price it in.

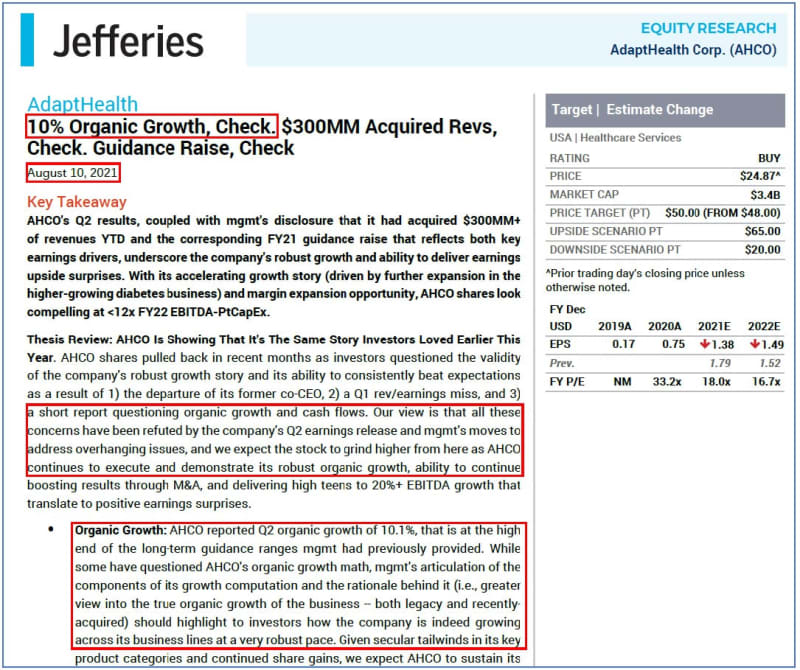

- Incredibly, the sell-side continues to miss this. Some members of the analyst community apparently didn’t even bother to open the 10-Q before putting out their follow-up detail notes. This kind of thing creates short opportunities for those who pay closer attention. Here is Jefferies with a note published after the Q2 10-Q was already available:

We aren’t highlighting Jefferies because we want to bash them. We’ve done business with Jefferies in the past and like the firm (and know they can do better than this). We picked out poor Jefferies to include in our report just as one example, to highlight the fact that so much of the market is, once again, oblivious to AHCO’s actual organic growth. But this time, the facts are right in front of us. We think the market will figure this out soon, with or without our help.

Street Numbers Haven’t Budged. They Implicitly Reflect 9%+ Organic Growth

- The 2022 guidance event is clearly at risk. For Q422, which is an entirely organic number, the Street is modeling 9% YOY growth. For 2023, also entirely organic, double-digit growth is forecasted. Management says organic growth is 8-10%, and the Street mindlessly plugs it in.

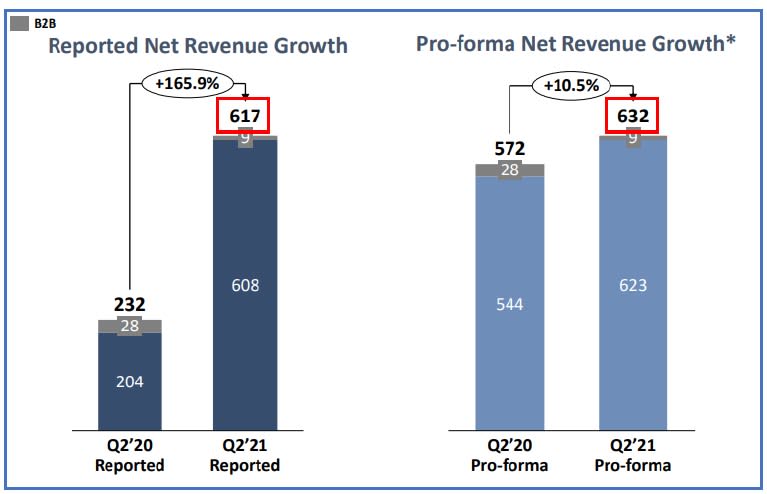

- We continue to believe that AHCO is sandbagging the inorganic contribution of its recently acquired businesses. For instance, with Spiro, it’s clearer than ever that this business is far bigger than management is claiming. This was suggested by the investor deck, but we needed the 10-Q to verify it. First, consider the pro forma information:

Q221 would have had $15m more in revenues ($632 vs $617m) had the Q221 deals been completed on the first day of the quarter.

Next, consider the disclosure about the Q221 deals in the 10-Q. This tells us that other than Spiro, the only other sizeable acquisition in the quarter was Healthy Living, a diabetes product provider. Diabetes providers command far higher multiples than regular HME providers like Spiro. Healthy Living was acquired on June 1 for $50m. If Healthy Living was purchased for the same multiple as Solara, another diabetes provider that AHCO bought for approximately 2x revenues, then it’s a $25m/year, or $6m/quarter, or $2m/month, business.

Healthy Living was bought on June 1, meaning it contributed one month to Q221. If Healthy Living is a $2m/month business, then including it since the first day of the quarter would have added $4m to Q2 revenues. Given the relative insignificance of the other deals in the quarter, this logic implies that the other $11m of the $15m pro forma addition is from Spiro. I.e., Spiro – bought on April 30 – would be an $11m/month business, or $132m a year.

In our original report, on page 15, we speculated that Spiro was a $122m per year business. We now have another data point suggesting about the same.

Why does this matter? Because management continues to say that Spiro, which was bought at the end of the fourth month of 2021, is going to contribute less than $40m to 2021:

*“The next \[guidance\] raise was the last call, we've talked about Spiro and there's also \-\- there is some dollars in there for the CMS oxygen fee schedule rate increases that were in effect April 1st, that was a $40 million raise…” *\\\- AHCO CFO on Q2 earnings call

If Spiro is a $122-132m business or anywhere close to it, it’s obviously going to contribute a lot more than “under $40m” in eight months…it would contribute more like $80m+ under this math.

To get right to the point: This kind of game is why management has been able to raise guidance in surprising ways. They buy a business doing X in revenues, they raise guidance by X, then they say the acquired business is only doing 0.5x, and the rest is…organic growth! Except it’s not. This is the “guidance raise” investors just bought on Q2 earnings.

- For how much longer can sell-side analysts look the other way on organic growth now that it’s plainly disclosed in the SEC filings? If you’re a client of an analyst who is modeling 8-10% organic growth, try asking him (and they are all “him”s) whether he’s read a 10-Q lately. Or, ask the new AHCO IR guy, who was a Buy-rated analyst at RBC until…about two weeks ago.

After Its Biggest-Ever Earnings Bounce Driven by False Promises, AHCO is Back to $24/Share!

- Our report catalyzed a (relatively) great deal of introspection by the sell-side on the question of organic growth, and drove investors to revisit their assumptions about this issue as well. AHCO’s stock price fell ~15% over the ensuing weeks as the investment community digested our claims and, apparently, found them compelling.

- When the company reported earnings and claimed, No, our organic growth is indeed 10%, the finicky market bid the stock back up to the mid-20s/share. As of now the stock price continues to approximate that level. Only three weeks after our report, the stock is back to the level at which it sat before anyone was questioning organic growth – because management “came out strong.”

- The only question now is, Who are you going to believe: Management, or your lyin’ eyes?

- We continue to believe that from the mid-20s, AHCO has approximately 50% downside (not much has fundamentally changed about this company in the few weeks since we last issued our price target).

- As of this writing, borrow cost for AHCO shares (reported by prime brokers to us) has fallen to GC levels – implying that the short interest has come down quite a lot as well, from already low levels.