The competitive threat fintechs pose to incumbent financial institutions has diminished in many regions over the past year. As capital has become more selective in the current rising interest rate, slower-growth environment, many fintechs, lacking the more stable funding of established institutions, have scaled back operations, especially those taking a ‘build now, profit later’ approach.

Among these are challenger banks N26 and Monzo, which exited the US market. Other unprofitable fintechs, such as buy now pay later (BNPL) company Affirm, have laid off staff, and a few have closed altogether. Surprisingly, some fintechs are still thriving, however. Below, a look at the main forces shaping fintechs’ current trajectory:

Q4 2022 hedge fund letters, conferences and more

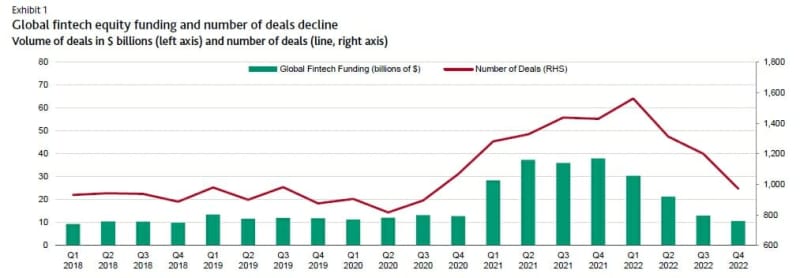

Unprofitable fintechs stumble as funding declines:

An unfavorable macroeconomic environment for growth investments has weakened fintechs and challenger banks, exposing many with flawed and uneconomic business models. In a higher interest-rate, lower-growth environment, venture capital and private equity firms have reduced funding that supported numerous new entrants.

The lack of capital has weakened fintechs, and in some cases caused their demise, including many that were not profitable and relied on existing banking architecture rather than offering a novel technology or product.

Incumbent banks have responded to the fintech threat:

Incumbents have made strategic investments to enhance digital offerings and expand their capabilities either organically or through partnerships or acquisitions. Incumbents also have a critical advantage in having well established brands and long customer relationships, giving them access to stable deposit funding that is particularly beneficial in a more difficult economic climate.

Regulation remains a continuing hurdle for fintechs:

In certain regions regulation remains a costly barrier to entry for fintechs seeking a foothold in financial services. In several developed economies, the climate for fintechs has become less favorable: regulators in Australia, for example, aim to tighten rules for BNPL, and in 2021 added requirements to the country’s licensing framework for new depository institutions.

Technology retains its potential to benefit and transform finance:

Longer term, technology’s capacity to lower costs, increase efficiency and broaden inclusion in financial services nonetheless remains. Some new entrants have done exceptionally well, and, although small, will no doubt continue to disrupt parts of the financial value chain.

Notably, fintechs that are part of technology conglomerates, such as KakaoBank, have generally fared better than those independents mainly funded through private capital.

Decline Of Venture Capital Funding Exposes Flawed Fintech Models

Venture capital funding sharply decelerated overall and especially for fintechs in 2022, exposing a long-standing weakness common to many of these new entrants to financial services: their heavy reliance on outside capital to fund their operations.

Many fintechs had negative operating margins and were focused on growth and building scale now, while achieving profitability and positive operating margins was a more distant goal. The decline in funding had more pronounced negative effects for those fintechs that were using capital to fund client acquisition costs rather than building and investing in valuable or unique infrastructure.

This type of fintech business model – relying on venture capital funds to subsidize user discounts that would help grow a customer base – is typically unsustainable.

Similarly, fintechs benefiting from regulation that allows them to charge higher payment fees have a more fragile business model than do fintechs that provide new delivery of financial services using more efficient technology. The sharp drop in funding for fintech firms in the past year has led to permanent closure of some startups.

Read the full report here by Moody's